Deciding between a 3-year or 5-year mortgage rate can greatly impact your financial situation. It's crucial to carefully consider both options before making a choice. Although Canadians commonly choose 5-year terms, 3-year mortgage terms have been gaining popularity in the hopes that the Bank of Canada will be able to curb inflationary pressures to avoid payment shock at renewal. Each term has advantages and disadvantages, but your choice should depend on the one that best suits your needs and circumstances.

Deciding Between a Fixed or a Variable Mortgage

Borrowers can choose between two main types of mortgages when financing their homes: fixed-rate mortgages and variable-rate mortgages. Lenders always offer 3-year fixed mortgage rates, 5-year fixed mortgage rates, and variable options for each term.

Fixed-rate mortgages offer a steady and predictable payment throughout the term, while variable-rate mortgages have interest rates that adjust based on lender prime rates. Both options have advantages, and borrowers must carefully consider their financial situation and preferences when determining the best fit.

Fixed-rate mortgages have a set interest rate that remains the same for the entire mortgage term. This means that your monthly payment will stay consistent throughout the term. This provides stability and predictability for the borrower, as the mortgage payment's interest and principal portions will remain unchanged until the end of the term.

Your monthly payments will remain unchanged if you have a variable-rate mortgage (VRM). However, the proportion of your payment that goes toward the principal and interest will change to accommodate any fluctuations in your lender's prime rate. If you have an adjustable-rate mortgage (ARM), your monthly mortgage payments will change whenever the interest rates change. The amount you pay monthly is determined by a fixed portion that goes towards the principal and a variable portion that adjusts based on your lender's prime rate.

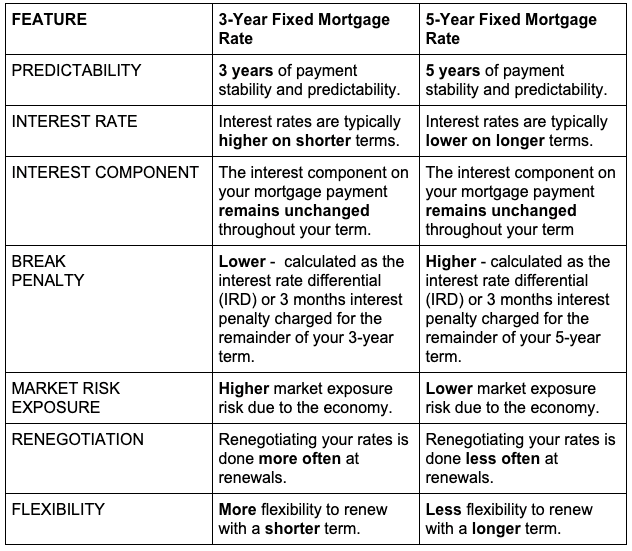

3-Year Versus 5-Year Fixed Mortgage

When deciding between a 3-year or 5-year fixed-rate mortgage, it's important to consider the current state of the market and what experts predict will happen in the future. Ultimately, deciding the best mortgage rate depends on your circumstances and preferences. It's important to carefully consider the mortgage rates forecast, market conditions and your own goals before making a final decision.

If the market indicates that interest rates are likely to continue rising, it might be a good idea to opt for a 5-year fixed term. Doing so can avoid re-negotiating a new rate in a few years when mortgage rates could be significantly higher than the one you initially locked into. This can provide you peace of mind and stability in the long run.

Choosing a shorter 3-year fixed term is a smart move if the market suggests that rates will decrease. This allows you to take advantage of a lower rate after 3 years, reducing interest-carrying costs. This option may also be more suitable if you plan on selling your property within the next 3 years, as it will result in a lower interest rate penalty (IRD) to discharge your mortgage than a 5-year term.

3-Year Versus 5-Year Variable Mortgage

Choosing between a 3-year and a 5-year variable mortgage can be a significant decision when financing your dream home. Both options offer flexibility for changes in your financial situation and a minimal interest penalty of 3 months to break your mortgage if your financial situation changes.

A 3-year variable mortgage offers a shorter commitment period, which can appeal to those who prefer flexibility and anticipate changes in their financial situation soon. With this option, you can reassess your mortgage terms and potentially take advantage of lower mortgage rates on a fixed mortgage or more significant discounts on another variable mortgage after the initial 3 years.

A 5-year variable mortgage locks you into a longer-term commitment. However, the interest rate on all variable mortgages can fluctuate during this period, so your monthly payments could vary on an adjustable-rate mortgage (ARM).

Shorter Versus Longer Mortgage Fixed Terms

Mortgage terms vary from as brief as 6 months to as lengthy as 10 years. The duration of your mortgage term will affect your interest rate since you have to renew after each term unless the mortgage balance is fully paid off. The most significant disadvantage to shorter terms is that they expose you to higher risk because market fluctuations affect you more. Additionally, you must renew or refinance to renegotiate your mortgage rate and terms more frequently.

Shorter-term mortgages have benefits, such as lower prepayment penalties if you need to break your mortgage early, as your penalty will be calculated on the time remaining until the end of your term. The same is true for longer terms, as you’ll need to pay higher prepayment penalties if you need to break your mortgage before the term ends.

Longer-term mortgages offer advantages, such as less risk exposure to market fluctuations as you’ll need to renegotiate mortgage terms and rates less frequently. Lenders often give lower interest rates for longer terms because they base their rates on longer-term bonds, which typically have lower yields when the economy is stable.

3-Year Mortgage Term

A 3-year fixed-rate mortgage is a good choice for those seeking a shorter time commitment. With this type of mortgage, you can benefit from a fixed interest rate for 3 years, meaning your monthly mortgage payments will remain the same throughout the term. This can provide stability and predictability for homeowners who prefer to have a set budget for a specific time.

If interest rates go down in the near future, getting a 3-year fixed-rate mortgage could be a smart move. It allows you to renew your mortgage at a lower rate when it matures without waiting an extra 2 years like you would with a 5-year rate.

However, there are some downsides to consider before deciding on a 3-year fixed-rate mortgage. If interest rates fall during the term, you can only take advantage of the lower rates if you pay a prepayment penalty to break your mortgage. This means that you may miss out on potential savings if rates decrease. Prepayment penalties for fixed-rate terms are generally higher than those for variable terms, so if you need to break your mortgage before the term ends, you will have to pay a higher penalty.

Since the rate is fixed for only 3 years, you may be more exposed to changes in the market. If interest rates rise after your term ends, you could face a higher interest rate when you renew your mortgage.

5-Year Mortgage Term

A popular choice among Canadians is the 5-year mortgage rate term. This option provides borrowers with stability and predictability by selecting a longer term. With a 5-year fixed-rate mortgage, borrowers can enjoy a fixed rate for the entire 5-year term. Many borrowers opt for this term due to the influence of conditioning and advertising by the country’s biggest lenders.

Canada's major banks, the country's top mortgage lenders, have shaped the financial planning landscape to favour the 5-year fixed-rate mortgage as the best choice. This term is widely advertised and often comes with more attractive pricing, as lenders offer significant discounts to secure clients for a longer period. Homeowners seeking stability and predictability over a longer period may find the 5-year fixed-rate mortgage appealing.

While a 5-year mortgage term offers benefits such as predictability and stability, it also has downsides. For instance, if interest rates decrease during the term, borrowers cannot take advantage of lower rates without facing substantial prepayment penalties. Additionally, being locked into a longer-term limits flexibility and the ability to make changes.

Despite these drawbacks, a 5-year term can be suitable for first-time homebuyers (FTHB) who need time to adjust to making regular mortgage payments. It can also benefit those anticipating interest rate increases and borrowers seeking consistency in mortgage payments.

Comparing 3-Year and 5-Year Fixed Mortgages

Choosing the correct length for your mortgage is pivotal for your mortgage strategy and helps you decide if switching lenders at renewal can save you money. It's essential to carefully consider your options and select the term that best aligns with your goals. By comparing 3- and 5-year rates and terms, you can evaluate how they fit into your short and long-term objectives, risk tolerance, and overall financial situation. This analysis will enable you to find a solution that suits your needs. Market conditions outlined by mortgage rate forecasts can also play a significant role in determining the suitability of a mortgage.

Shopping for a Mortgage in Canada

When searching for mortgage rates in Ontario, Quebec, Alberta, or anywhere else in Canada, rate comparison websites can simplify your search by allowing you to compare different mortgage options and find the most suitable one for your needs.

Instead of visiting multiple lenders or scouring numerous websites, you can use these tools to compare your options easily. With CompareMortgages and MonMeilleurTaux, you can assess each mortgage offer, enabling you to make decisions more quickly - saving you time and effort when shopping for a mortgage.

This can assist you in finding the best mortgage for your situation, whether you're purchasing a home or renegotiating your mortgage rates in Montreal, Calgary, or Toronto.

Discussing your financial situation and mortgage needs with a mortgage expert is highly recommended to ensure you make the best decision for making yourself mortgage-free faster. They can provide valuable insights and help you complete a cost-benefit analysis, allowing you to make a well-informed choice that aligns with your unique circumstances. Reach out to one of nesto's mortgage experts, who can assist you in determining whether a 3 or 5-year mortgage term is the right choice for you.